Meanwhile … have insurers ratted out freeholders and the large managing agents by offering up their commissions as a contribution to the building safety crisis?

At last the government seems to have lost patience with the cosy leasehold insurance racket, whereby freeholders, their managers, brokers and insurance companies more or less charge what they like to insure a block of flats knowing that the leaseholders who do the paying will never know the commissions that are involved.

Price gouging of insurance in flats caught up in the building safety crisis has prompted the move.

In addition, it looks like the Association of British Insurers is finally poised to rat out freeholders and managing agents who take obscene commissions gaming leasehold insurance.

These commissions need to be on the table in any sector-wide contribution to pay for building safety defects, the ABI has said.

At present, punters in residential freeholds – nowadays private equity and often anonymous and offshore – are paying nothing to remediate “their” buildings, in spite of a lot of public relations hot air about being “professional long-term guardians” of blocks of flats.

At the Communities Select Committee last week Florence Eshalomi, the Labour MP for Vauxhall, asked James Dalton, of the Association of British Insurers, whether his members should contribute to building remediation given the profits they have made hiking insurance costs across the sector.

An uncomfortable Mr Dalton replied:

“One of the significant costs in the price of insurance is commission. If we are going to do anything to reduce the costs that fall on leaseholders all things need to be on the table. And my submission to you is that commission and distribution should be one of them.”

On January 28, Communities Secretary Michael Gove unleashed the more aggressively pro-consumer Competition and Markets Authority (annual budget: £91 million), which has a track record of defending leaseholders, against the Financial Conduct Authority (annual budget: £632 million) to sort out the insurance of blocks of flats.

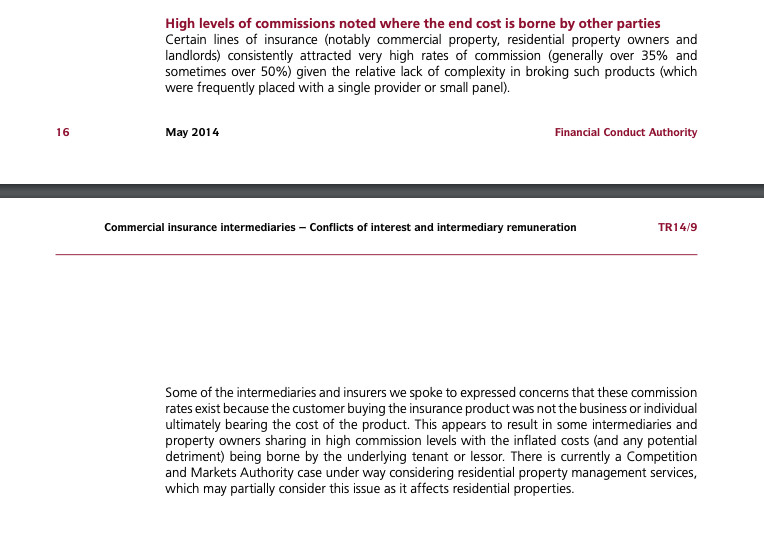

The FCA acknowledged as far back as 2014 that leasehold insurance can involve commissions “generally over 35% and sometimes over 50%”.

Last summer LKP demonstrated how Rendall and Rittner, generally regarded as one of the more sophisticated operators in the sector, was obtaining a 40% return on the premium paid by leaseholders – not by charging commissions, but by running an offshore captive re-insurance company:

Artex, the offshore re-insurer used by Rendall and Rittner could not be more blatant: using a captive insurer is just a work-around as the temperature around dodgy commissions is too hot involving the CMA and even ARMA-Q, the enhanced ethical guidelines for managing agents.

It even produced a document, referenced in the article above, “An Alternative Approach to Commission for Property Owners & Managing Agents”. It says:

“Managing insurance placement on behalf of tenants can be an important revenue stream of commission-based income for both property owners and managing agents. Many organisations are making strategic decisions to move away from risk-free income in response to commission disclosure proposals which has resulted in an increasing demand to create innovative structures that allow revenue to be generated from block insurance policies. “Proposals include the OFT and CMA studies and the release of ARMA-Q”

It would be ludicrous to believe that other managing agents and freeholders are not using the same arrangement, and that UK insurers are well aware of this.

In a letter to the FCA on January 28, Mr Gove said:

“I have been extremely concerned to hear from innumerable leaseholders about the pressure they face from rapidly escalating building insurance premiums on high and medium-rise blocks of flats. I have been particularly concerned to hear of cases where insurance premiums have escalated by over 100% year-on-year, leaving residents with crippling costs. It is clear to me that the insurance market is failing some leaseholders …

” … building insurance premiums have increased dramatically for almost all leaseholders in blocks of flats. I am also concerned to hear that many insurers seem unwilling to offer new policies, forcing people to shop in a more limited market place with more restrictive terms or less coverage; in many cases, trapping people with their current provider.

“Understandably, many policyholders do not view the market as effectively delivering accessibly priced, widely available insurance. I share that view, and do not consider this an acceptable situation.

“The market lacks transparency and there is not currently useful data to explain the rationale behind the increasing premiums charged by insurers and the conditions associated with the cover.

“The role and remuneration of brokers, managing agents and freeholders is also unclear. I require urgent advice on the scale and potential causes of the problem and what can be done to rectify these issues. My overall goal is for there to be a more affordable marketplace for buildings insurance that offers widely available and affordable cover for those who live in flats and other multiple-occupancy buildings.”

The FCA replied the same day, delicately indicating that insurers have to assess risk (omitting to add that the government itself had made this more difficult by the consolidated advice notice that gave birth to EWS1 surveys and findings that virtually every block of flats built in the last 20 years had serious building safety defects.

The FCA wrote immediately to insurance company CEOs, in characteristically feeble fashion:

“While firms often do not treat leaseholders as the customer, it is leaseholders who are likely to pay for the policy and benefit from it. When determining what is fair value, what is in the best interests of customers and what meets their needs, firms should take into account the freehold property owner and the freehold property owner’s duties to their leaseholders.”

There follows more in the same vein – “distributors must not be influenced to act against customers’ best interests by commission or other remuneration” – but lacking from the FCA is a clear instruction that leaseholders who do the paying are a party to the insurance contract and can clearly see all its terms, which is what LKP has been urging for years.

Delaware Department Of Insurance Loses IRS Summons Fight For Artex And Tribeca Captives But Can Appeal

I have previously written about the lawsuit filed by the U.S. Department of Justice to enforce an IRS summons directed to the Delaware Department of Insurance (DDOI) for its e-mails and other documents relating to the investigation of Artex Risk Solutions, Inc. (which is affiliated with Arthur J.

It is absurd to pretend that Rendall and Rittner’s imaginative offshore insurance arrangement is a one-off. Reaping the insurance bills is one of the premier perks of being in the leasehold business.

The CMA chief executive Andrea Coscelli reponded to Mr Gove saying that the CMA was happy to get stuck in and “strengthening our understanding of what is driving high premiums will be key to taking effective action to protect residents”.

Back in 2014 the CMA had called on freeholders and their agents to disclose insurance commissions, but the FCA did nothing.

https://www.insurancetimes.co.uk/property-managers-to-disclose-broker-commissions/1411091.article

Last November, Mr Coscelli responded to a letter by LibDem politicians Sarah Olney MP, Lord Newby and Cllr Rabina Khan urging the CMA to intervene over secret insurance commissions:

“It is clear, not least from the complaints that the CMA itself has received, that many leaseholders have suffered significant financial loss and emotional distress over a number of years. To the extent that it is able, the CMA will act directly to assist leaseholders that have experienced detriment; and it stands ready to advise and assist government as it responds to this important issue.”

Related posts:

Michael Gove: Is this the robust inquiry into leasehold insurance fiddles that you wanted from the FCA?

Michael Gove: Is this the robust inquiry into leasehold insurance fiddles that you wanted from the FCA?

Insurance insiders call for an end to secretive leasehold insurance commissions following Canary Riverside ruling

Insurance insiders call for an end to secretive leasehold insurance commissions following Canary Riverside ruling

Financial Conduct Authority under pressure to force open secretive insurance commissions, so leaseholders can see what they are paying for

Financial Conduct Authority under pressure to force open secretive insurance commissions, so leaseholders can see what they are paying for

Leaseholders pay up to 60% more for buildings insurance because of secret commissions, reports The Times

Leaseholders pay up to 60% more for buildings insurance because of secret commissions, reports The Times

LKP urges minister to include leaseholders in Flood Re insurance plan

LKP urges minister to include leaseholders in Flood Re insurance plan

Morello Quarter leaseholders stall ruinous cost of waking watch, but how useful is court decision for others?

Morello Quarter leaseholders stall ruinous cost of waking watch, but how useful is court decision for others?