Do you think leasehold insurance costs are fair? No? Surprising that. The FCA wants to hear from leaseholders as part of its consultation to ensure that this market is opened up:

https://www.fca.org.uk/publications/consultation-papers/cp23-8-multi-occupancy-building-insurance

The Financial Conduct Authority – following robust prodding from Michael Gove and years of pushing by LKP and its patron Sir Peter Bottomley – has found “significant shortcomings” in the leasehold insurance racket.

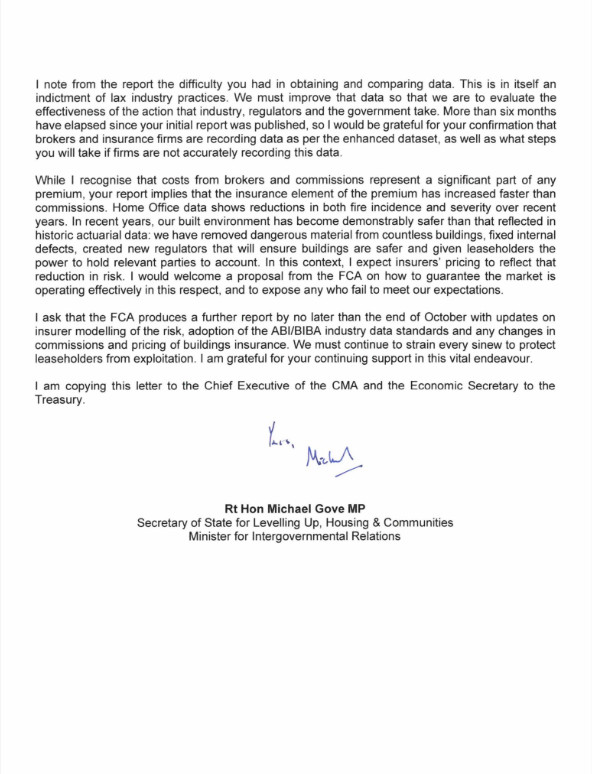

Michael Gove has told the FCA:

“I was, in all candour, outraged by your findings. You have found that broker remuneration has risen by nearly 40% in the last three years, with £80m of commissions going to other parties – and that brokers are unable to provide any evidence to demonstrate that this represents fair value. Despite this, they are happy to load these unwarranted and opaque costs on innocent leaseholders.”

But in spite of repeated by LKP and Sir Peter that the problem is the placing of insurance by unaccountable freehold owning landlords, the emphasis of the FCA report is on insurance brokers.

Fighting inflated insurance involves leaseholders in wars of attrition with their landlords, notably Canary Riverside in London’s docklands:

The FCA report highlighted “deficiencies in [brokers’] product value assessment work, shortcomings in their recording and analysis of their own costs and insufficient scrutiny of the commissions they pay to others”.

It was “likely” that brokers would need to reduce their percentage-based commission rates if they could not demonstrate a sufficient benefit to customers.

Enforcement action leading to fines and bans is mentioned, but the FCA suggests no cap on commissions, citing “practical concerns” given the varying split of responsibilities between brokers and freehold-owing landlords. The latter do not fall within the regulator’s remit.

Michael Gove, however, correctly returns to soaring premiums in his letter:

“While I recognise that costs from brokers and commissions represent a significant part of any premium, your report implies that the insurance element of the premium has increased faster than commissions. Home Office data shows reductions in both fire incidence and severity over recent years. In recent years, our built environment has become demonstrably safer than that reflected in historic actuarial data … I expect insurers’ pricing to reflect that reduction in risk …

“I would welcome a proposal from the FCA on how to guarantee the market is operating effectively in this respect, and to expose any who fail to meet our expectations.”

Martin Boyd, chair of the Leasehold Knowledge Partnership, said he was pleased the regulator had “accepted something that we have argued for 10 years [was] a problem.”

Mick Platt, managing director of the Wallace group and director of the freeholders’ lobbying group the Residential Freehold Association, said it welcomed the move “to improve the transparency of the multi-occupancy leasehold buildings insurance market”.

That’s a change of tune from Gary Murphy, of Allsops, talking up the attractions of resi freeholds to potential punters because you did not have to divulge commissions to leaseholders.

Outrageously, Mr Murphy set out his case at a conference organised by the taxpayer-funded Leasehold Advisory Service:

Related posts:

Michael Gove: Is this the robust inquiry into leasehold insurance fiddles that you wanted from the FCA?

Michael Gove: Is this the robust inquiry into leasehold insurance fiddles that you wanted from the FCA?

Gove calls on complacent FCA to stop the leasehold insurance rip-offs, and urges the CMA to get stuck in as well

Gove calls on complacent FCA to stop the leasehold insurance rip-offs, and urges the CMA to get stuck in as well

Insurance insiders call for an end to secretive leasehold insurance commissions following Canary Riverside ruling

Insurance insiders call for an end to secretive leasehold insurance commissions following Canary Riverside ruling

Note to Mr Gove: FSA was warning of ‘reputational risk’ in not cracking down on secret leasehold insurance commissions 17 years ago!

Note to Mr Gove: FSA was warning of ‘reputational risk’ in not cracking down on secret leasehold insurance commissions 17 years ago!

Galliard and Lendlease were quick to get leaseholders on the hook for building safety bills, now they won’t sign Michael Gove’s agreement to pay up

Galliard and Lendlease were quick to get leaseholders on the hook for building safety bills, now they won’t sign Michael Gove’s agreement to pay up

Interview with Lord Greenhalgh: I don’t think the leasehold reforms will be in the King’s Speech

Interview with Lord Greenhalgh: I don’t think the leasehold reforms will be in the King’s Speech

The ONLY reason there is no transparency is because it suits the various parties involved. Since leaseholders are not party to to contract they have no say.

The parties to the contract COULD disclose commissions and other fees but they choose not to do so. They will have to be forced into doing so.

The FCA could do this this by adding rules forcing full disclosure on brokers AND insurance companies on all such contracts, irrespective of who gets any commission. This would bypass the freeholders and managing agents who are the bad boys here, as usual.

I’m quite impressed that Gove does seem to be getting a real grip on this.

Good on the Rt Hon Micheal Gove.

Insurance commission is just another way leaseholders are being scammed, and further draws attention to the failure of Codes of Practice regarding transparency and integrity!

Our managing agent only revealed that he took a 10% commission very reluctantly and only after ordered by the First-tier Tribunal to do so and after I pressed the matter. But I was not convinced that all had been revealed, as the Tribunal was feeble and tried to defend the status quo and the managing agent for some reason or other best known to itself. As the insurance for our block/house is lumped in with that for other properties for which the managing agent acts, everything is left obscure. The whole insurance system needs opening up.

Absolutely. 👍

Even the R.I.C.S. Residential Management Code of Practice says –

leaseholders should be notified annually of any remuneration, commision and other sources of income and related income or other benefits received in connection with placing or managing insurance

As said, this insurance commisions scandel further draws attention to the extensive failure of Codes of Practice despite Parliamentry approval of said Codes!